U.S. corporate borrowers are facing major refinancing risk in the coming years — at a time when funding costs are the highest in 13 years, Moody’s Investors Service said Thursday.

Stubborn inflation is keeping interest rates elevated, meaning companies will have to pay up when they roll over debt.

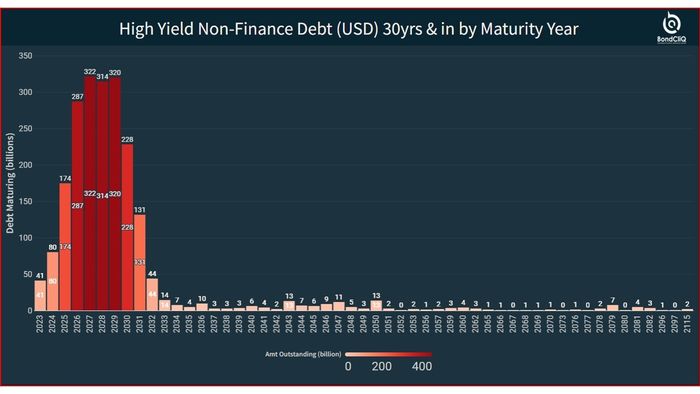

Issuers of nonfinancial speculative-grade, or high-yield, debt have a record $1.87 trillion of debt maturing in the period running from 2024 to 2028, the ratings company said in a new report. That’s up 27% from the previous record of $1.47 trillion of debt that matures between 2023 and 2027, published in last year’s report. Moody’s has published 26 reports on refinancing risks and the needs of U.S. speculative-grade issuers.

The looming maturity cliff is raising default risk and contributing to rising default rates. Moody’s is expecting the U.S. speculative-grade default rate to peak at 5.6% in January of 2024, before easing to 4.6% by August 2024.

The increase stems partly from large 2028 maturities, most of which are leveraged loans. It’s also due to the first-time addition of debt issued by non-U.S. subsidiaries.

The 2028 maturities total $560 billion after record issues of leveraged loans in 2021, which typically have tenors of seven years.

“These increases exceeded the declines in maturities resulting from refinancing, debt repayment and rating upgrades to investment grade since last year’s study,” Moody’s said. “High interest rates and constrained market access limited the amount of refinanced debt ($414 billion) and new issuance ($242 billion) since last year’s study.”

Read also: An ‘iceberg’ awaits with only 10% of the junk-bond market feeling the pinch of higher rates, says BofA Global

The “pull-forward” effect and “amend-and-extend” activity is amplifying refinancing risk for leveraged loans, according to the report.

“Companies’ tendency to refinance several tranches of debt in a single bank credit agreement when the first tranche, typically a revolver, comes due could more than double their 2024-26 bank debt maturities to over $1 trillion, representing 80% of the total five-year bank maturities,” the report said.

Adding to the overall risk, there’s more debt maturing from lower-rated issuers than usual, with the single B category accounting for 62% of total maturities, Moody’s said. The lowest-rated issuers, those rated Caa to C, hold 11% of maturing debt.

“Debt from distressed companies — those rated Caa and lower — accounts for 19% of 2024-25 maturities, up from 16% due in the first two years of last year’s study,” Moody’s said. “Companies rated Caa and lower will likely find it difficult to refinance maturities at an interest rate they can afford.”

By sector, technology, media and telecom companies have the most maturities, at 23% of five-year maturities, followed by services with 22% of maturities.

The following chart from data-solutions provider BondCliQ Media Services shows just how steep the approaching cliff has become. And high-yield issuers were able to sell debt at interest rates of 5% or less during the long period of zero interest rates that preceded the current rate-hike cycle, but they are now having to pay up to 12%.

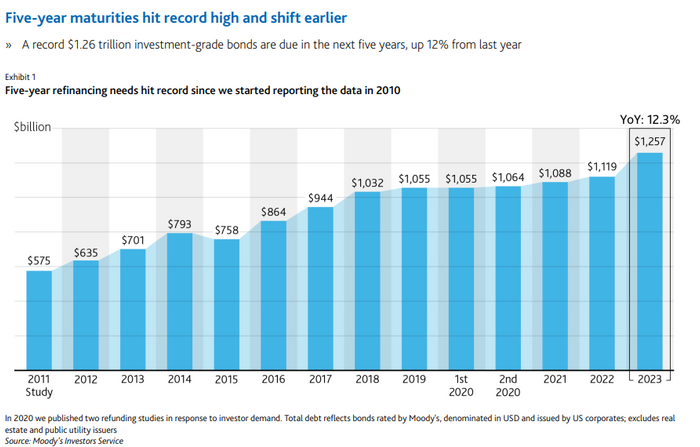

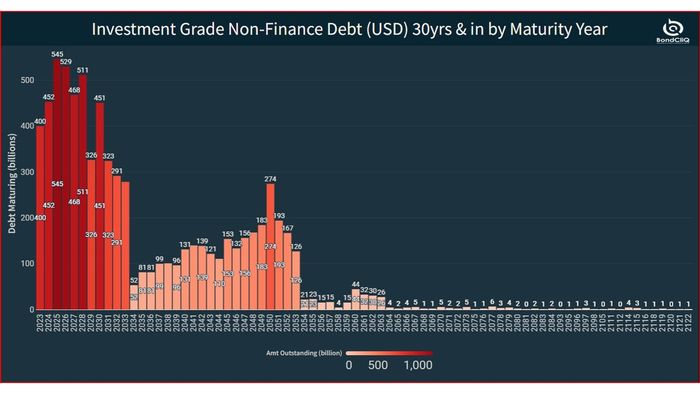

In the investment-grade world, meanwhile, refinancing risks are rising as five-year maturities for nonfinancial investment-grade bond issuers are up 12%, at about $1.26 trillion of debt coming due between 2023 and 2028. The bulk of that comes due in 2025.

“Still, we expect IG companies to maintain good bond market access and have sufficient cash flow to absorb higher interest costs,” the Moody’s analysts said.

But higher-for-longer interest rates will raise funding costs and are a credit negative.

In response, companies are shortening tenors on new debt and seeking to reduce duration risk.

As of September, investment-grade issuance has climbed 20% from the year-earlier period.

“The proportion of maturities within the first three years of our five-year scope increased to 61%, compared with 58% last year, pushing refinancing risk earlier,” said Moody’s.

Read: A wrecking ball could hit leveraged loans if the Fed keeps rates high

Also: Corporate bonds are on sale. How to add cheap Apple, Disney and Microsoft bonds to your portfolio.

Read the full article here