The layout has been adjusted to lead with the tickers and charts. Why? Because I think it allows the article to flow more naturally. Like it or hate it? Let me know in the comments.

The High Yielders

The charts compare the common shares from the following mortgage REITs and BDCs:

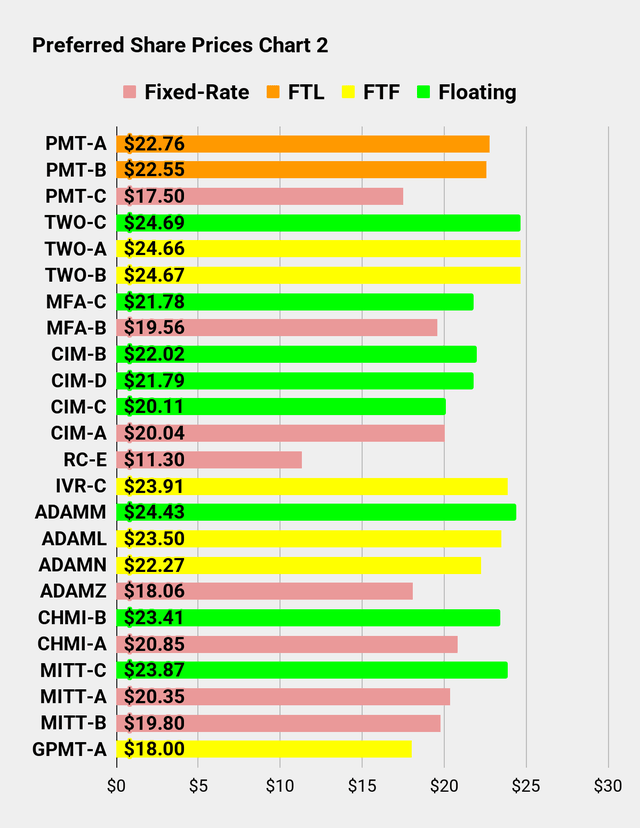

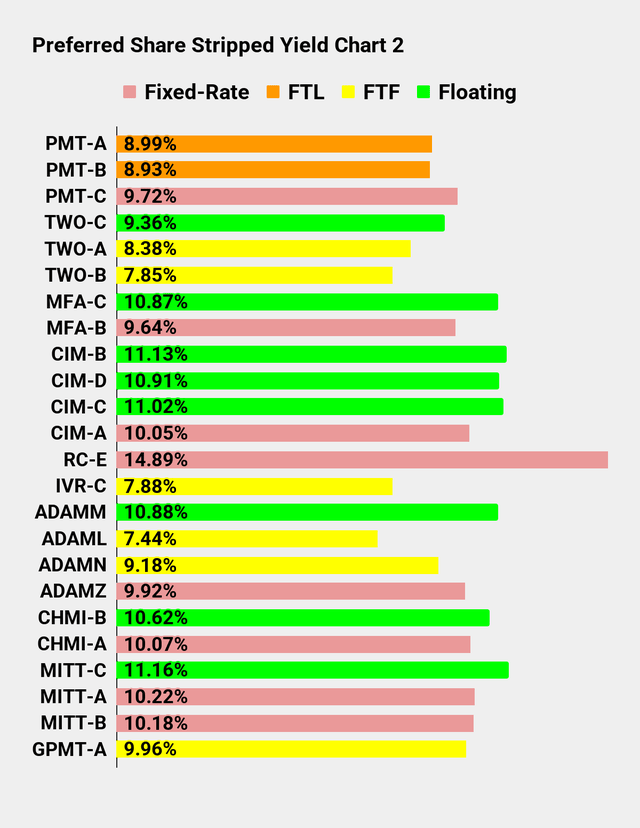

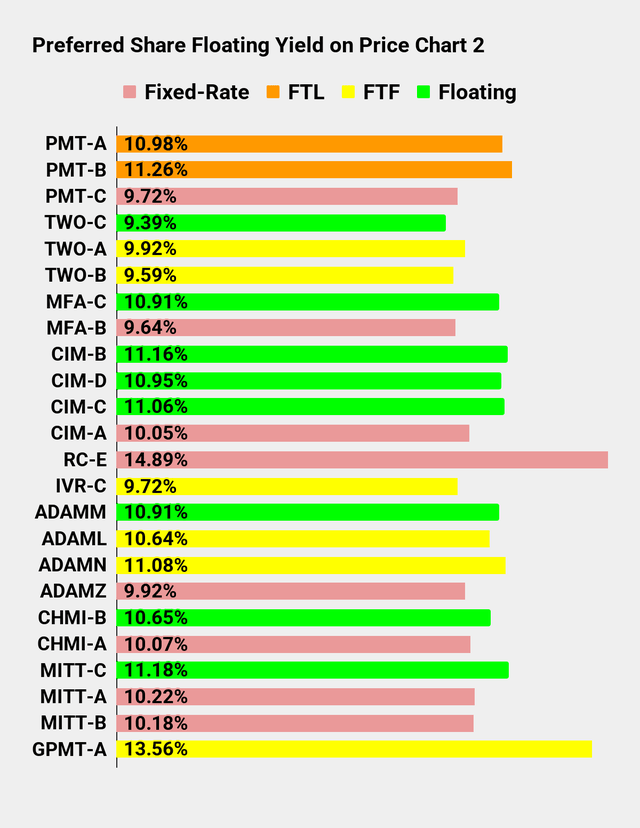

The Charts

Mortgage REITs and BDCs:

Preferred shares and baby bonds:

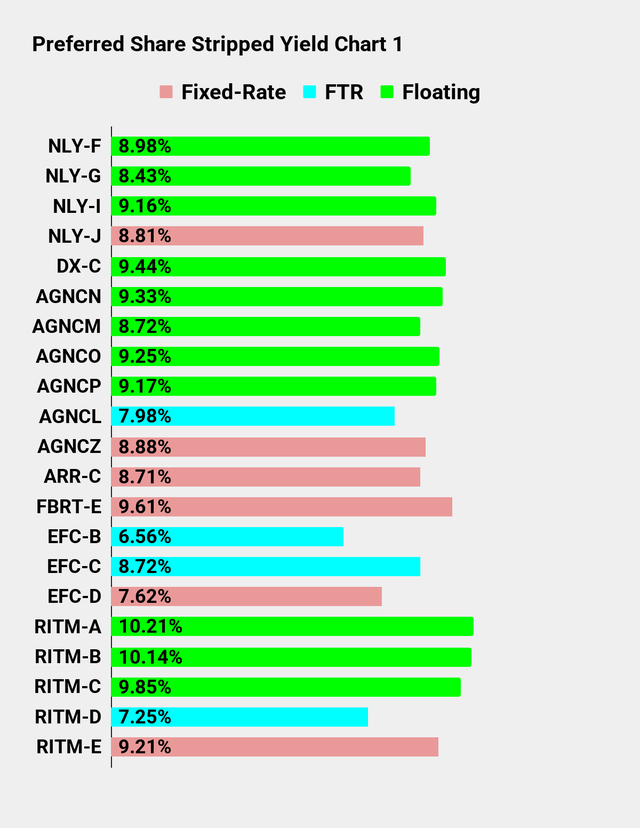

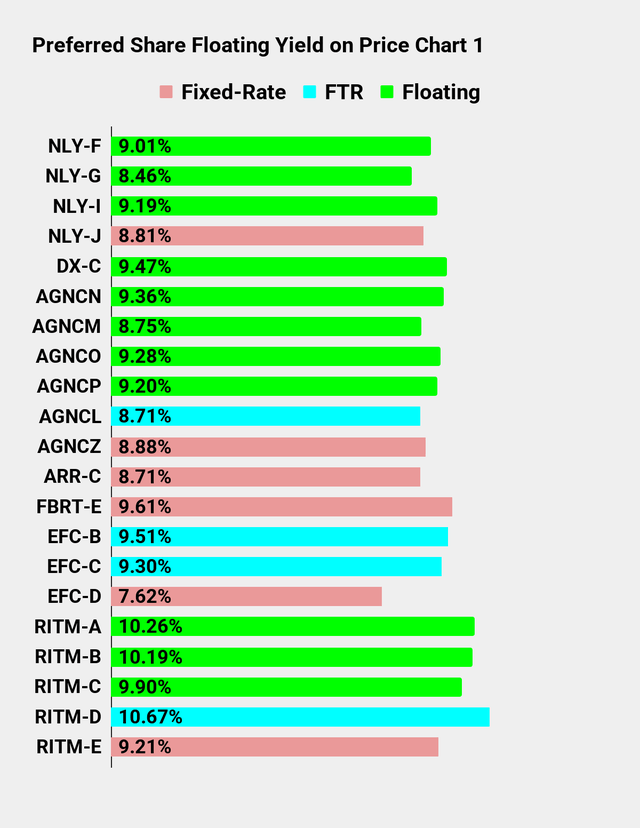

Definitions for preferred shares:

- FTF stands for “fixed-to-floating”. It means the share is fixed-rate, but will begin floating based on SOFR. We may still refer to LIBOR, but LIBOR simply means SOFR + 26.161 basis points.

- FTR stands for “fixed-to-reset”. These shares are currently fixed-rate, but will eventually reset their dividend rate based on the 5-year treasury rate plus a given spread. They typically continue to reset every 5 years thereafter. At least in theory. That’s pretty far away, but those are the terms.

- FTL stands for “fixed-to-lawsuit”. It only gets applied for PMT because they were the only mortgage REIT (that we know of) where management announced that “floating” really means a fixed dividend rate that never changes. PMT was sued over their actions. If you’re not familiar with it, see this article on the lawsuit.

- Floating stands for a share that is floating. Pretty obvious, right? This is the adult version of “FTF”. The rate is typically updated every 3 months.

Commentary From The REIT Forum

It’s been way too long since I posted this series. I apologize for the delay. As you may have heard, the market has been a bit volatile. I’ve been quite active in trading over the last several weeks as we build our positions. The higher interest rates are a substantial headwind for some of the securities we cover, but can even be favorable for some of the others. My favorite area for purchasing lately has been the floating-rate preferred shares and baby bonds. We cover many of them on The REIT Forum, as you could guess from the charts above.

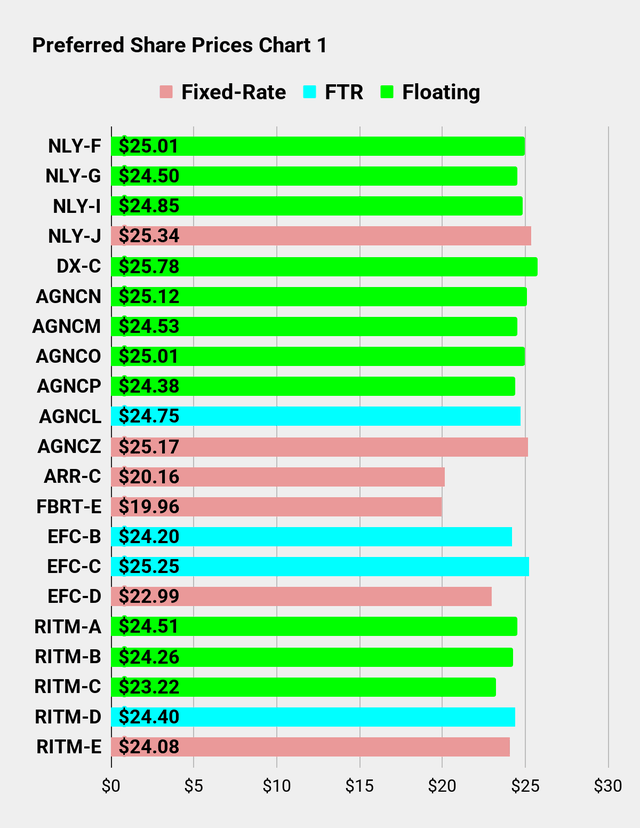

Preferred Shares

The floating-rate preferred shares can be appealing because many are now trading at a nice discount to call value. With fewer projected cuts to the Fed Funds Rate, these preferred shares are looking at higher dividends. So, what pushes the price down? Well, credit spreads have been widening. As the market sees increasing risks, credit spreads go up. I think we have some nice opportunities in the sector now, so I’ve been building those positions.

When the market was less concerned about risk, we saw quite a few of these shares achieve prices high enough to make the yield-to-call negative. Now opportunities are opening up again.

We recently mentioned initiating a position in NLY-I (NLY.PR.I). Share values declined since then, but only slightly. As we predicted, there was healthy demand sitting around $25.00. Shares are down, but only to $24.88, because investors find the yield (about 9.15%) quite appealing, and preferred shares under $25.00 tend to gather more attention.

NLY-F (NLY.PR.F), which was frequently overvalued (severely negative yield to call), now has an 8.2% annualized yield to call.

While the lower-risk preferred shares like those from Annaly Capital Management are only down slightly, we’ve seen much larger declines in some of the higher-risk shares.

Following the dip in baby bonds, there is only one preferred share (in this sector) that still has a negative yield to call. That would be DX-C (DX.PR.C). Management is careful and has done a solid job with the portfolio. Yet the preferred shares carry a floating-rate dividend that includes a 5.461% spread. That’s too large relative to the actual risk, so investors bid for the shares until they drive the yield-to-call negative.

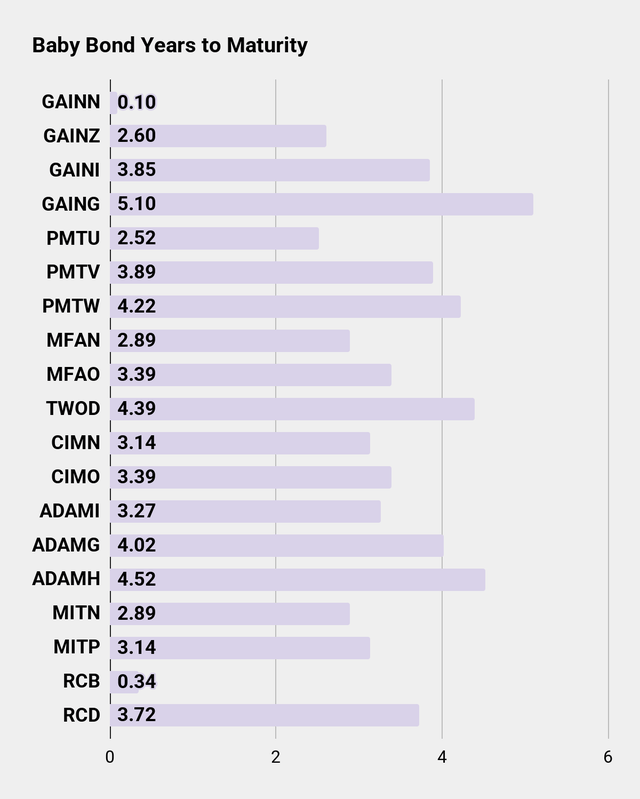

Baby Bonds

The nice thing about the baby bonds is that the maturities are not all that far off. Consequently, even a material increase in Treasury yields doesn’t move the price that much. If the bond matures in 3 years and Treasury rates rise by 33 basis points (such as 3.73% to 4.06%), it only merits a decline in the price of about 1%. That results in much lower volatility for the portfolio. So when I spot baby bonds going on sale with yields to maturity around 10%, that’s pretty attractive. We’re looking at big coupons combined with a modest gain for reaching maturity. I waited a few months for some of these opportunities to show up and they are finally here. So I’m happy to be able to build those positions.

Relative Value

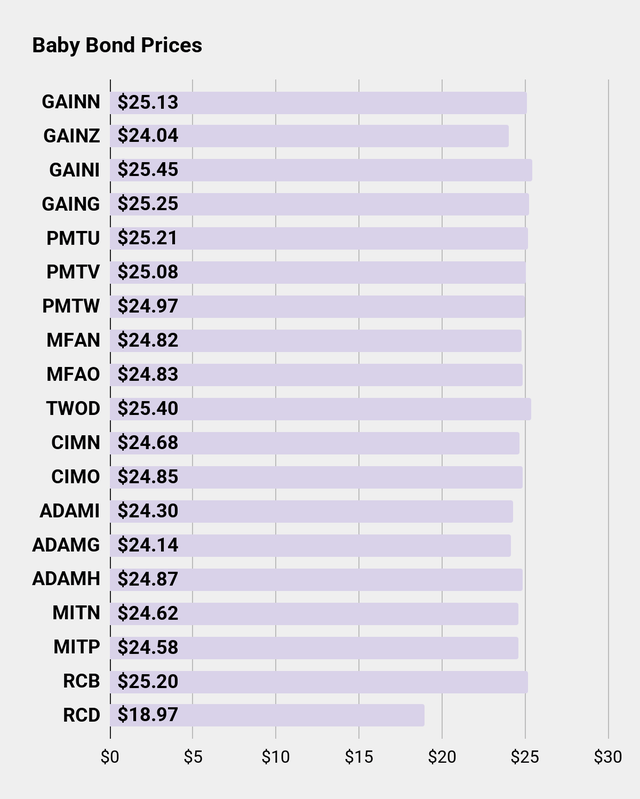

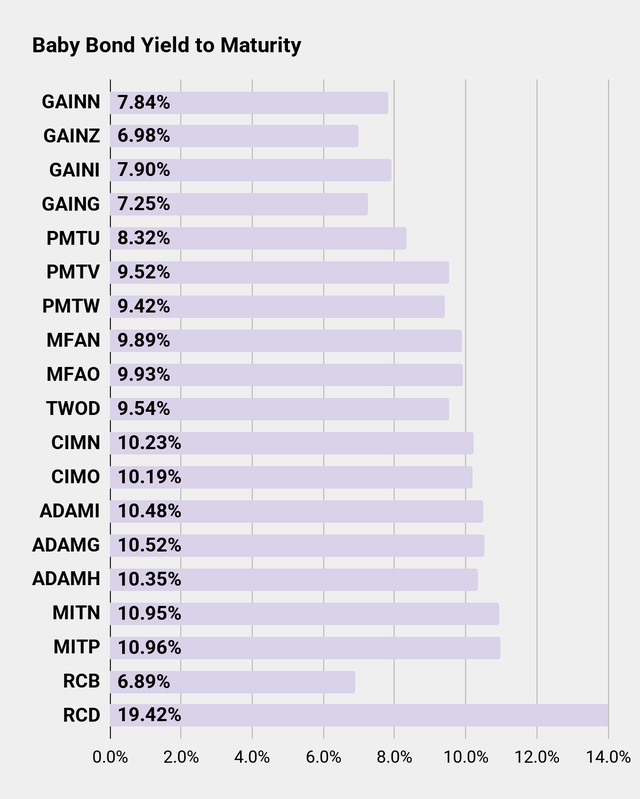

To demonstrate the spread in relative values, I like using this image:

The REIT Forum

The only advantage for PMTU is the earlier maturity. It matures in late 2028, rather than early 2030 or mid-2030. In exchange for that, investors get more call protection, a vastly better yield to call, and pick up 120 basis points on yield to maturity.

There are two main scenarios for the next 2.5 years:

- If PMTU gets called, then we are most likely dealing with lower interest rates and thinner credit spreads. In such a scenario, PMTV and PMTW would probably trade at a nice premium. That clearly favors PMTV and PMTW over PMTU.

- If PMTU is left outstanding until maturity, then PMTV and PMTW will have collected an extra 110 to 120 basis points in yield to maturity over that time. But what if the prices of PMTV and PMTW went down? If PMTV and PMTU underperform over the next 2.5 years, their prices must be down by more than 1%. That would give them a pretty high yield to maturity for the final stretch. It’s not impossible, but it is improbable.

This is a pretty common failing in the market. It has regularly overvalued PMTU relative to the other two baby bonds.

Since I’m mentioning these baby bonds, I need to mention that they have different ex-dividend dates. That’s pretty strange. Most REITs design their baby bonds to have the same ex-dividend date. Consequently, in any analysis comparing the baby bonds, you also want to consider dividend accrual. Currently, PMTV has the most with $.35. PMTW is in second place with $.18. The difference of $.17 in dividend accrual enables PMTV to be more attractive even though the share price is higher by $.11.

Common Shares

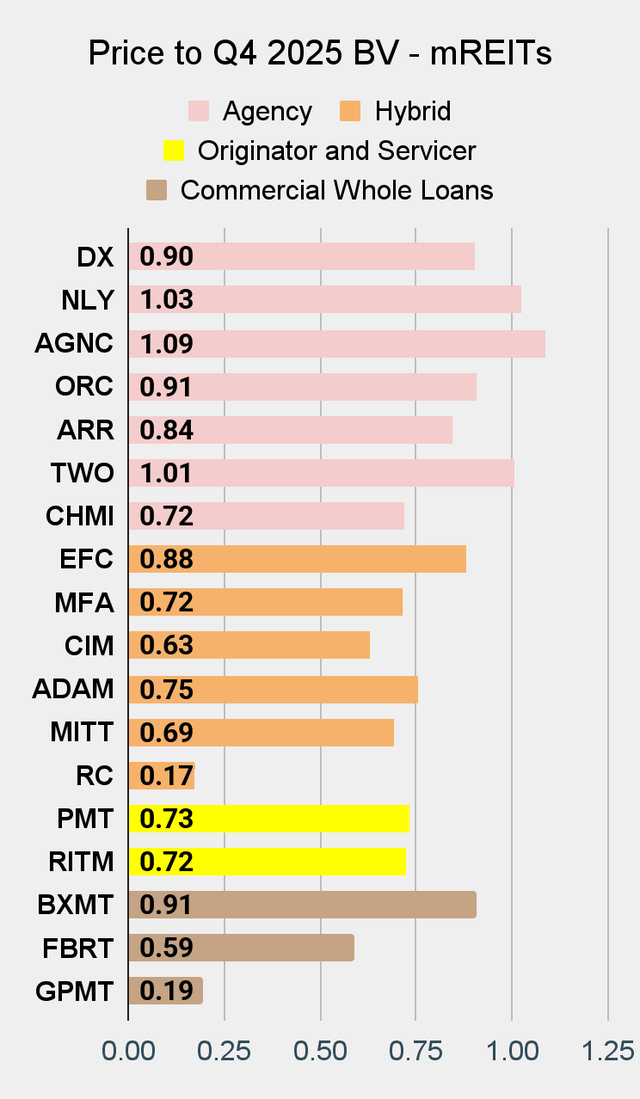

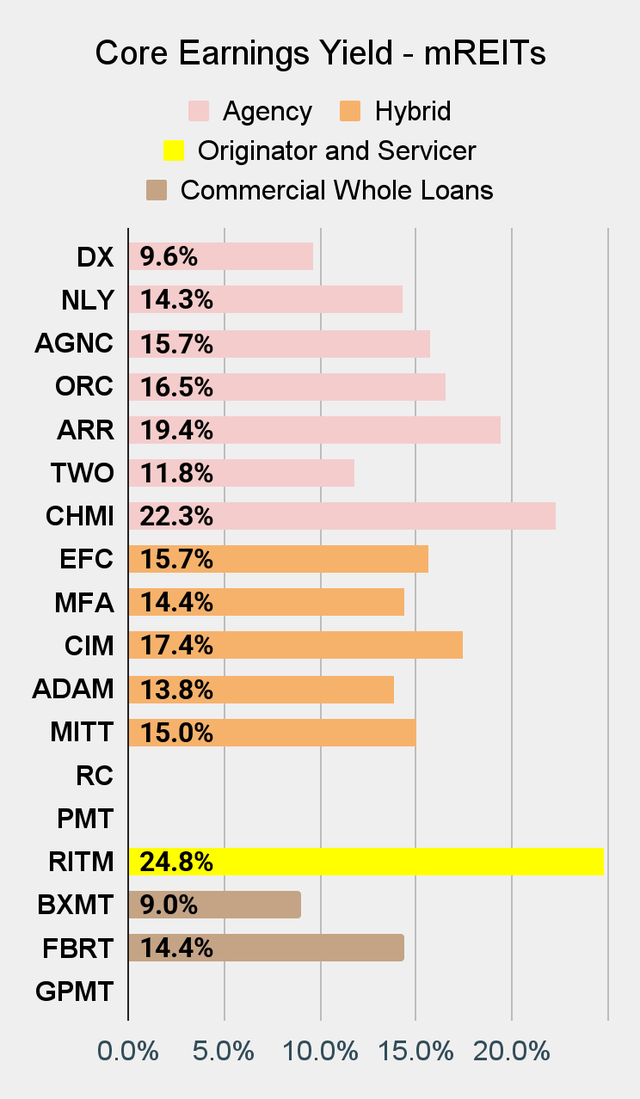

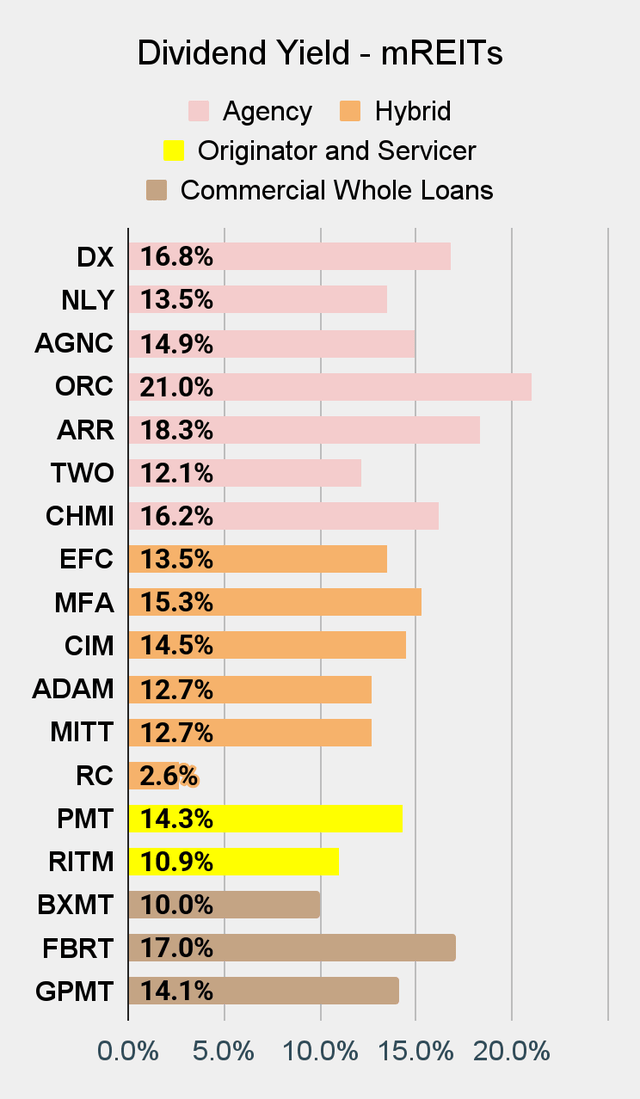

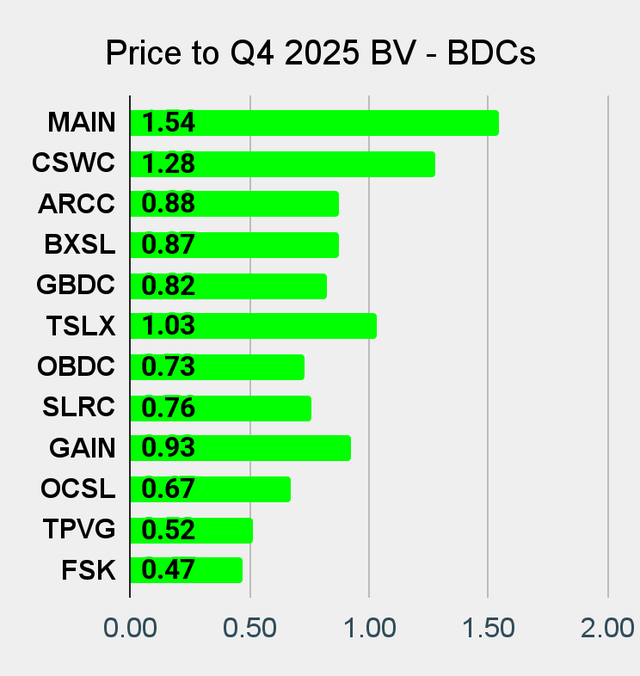

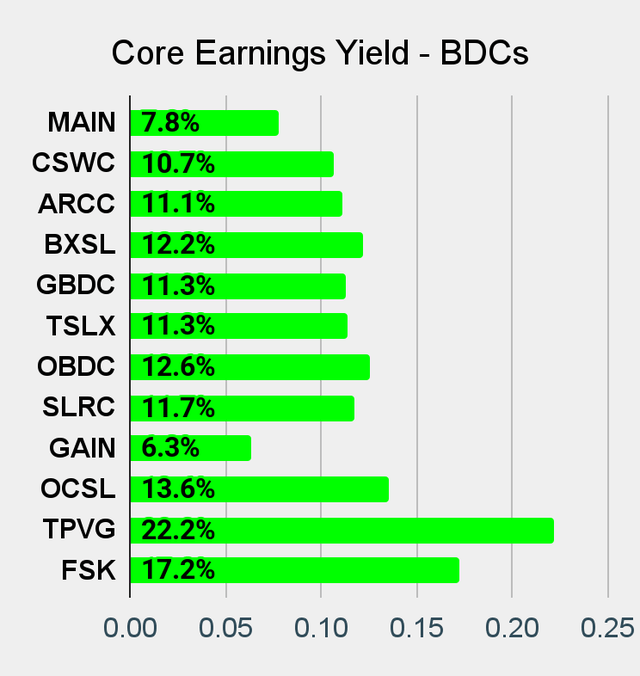

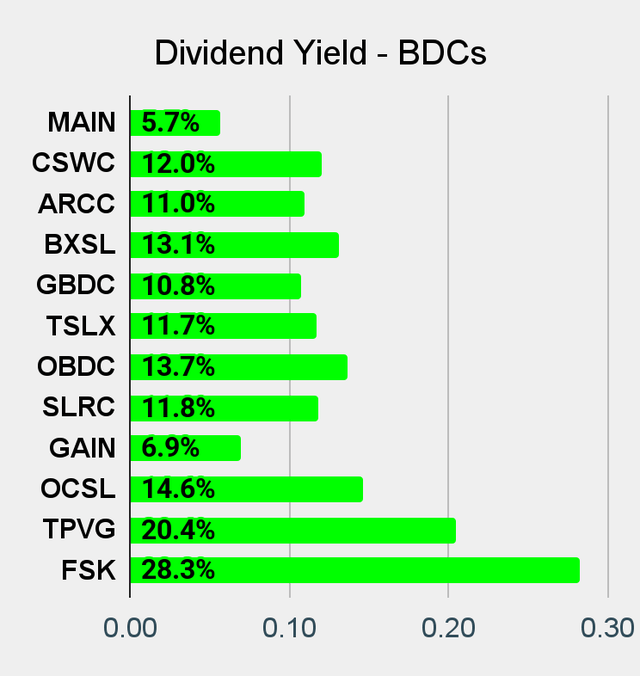

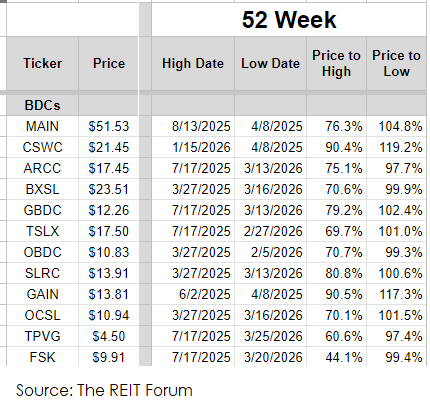

If you’re in the mood for the even higher-yielding common shares, the valuations are finally coming back down. Many of the mortgage REITs are down 15% to 18% from their 52-week highs. The BDCs are down much more though. I pulled a few of the columns from one of our sheets for subscribers to demonstrate:

The REIT Forum

This image really isn’t doing the sheets justice. But the goal here was simply to communicate the information quickly. It did the job.

We saw quite a few BDCs setting fresh 52-week lows today. My BDC allocation is pretty small and it’s doing alright overall. I didn’t start purchasing until the sector was getting pounded. My biggest loss in the BDCs is down about 12.5%. Yes, it’s down, but that was the worst-performing BDC purchase. Some of my positions in the sector are still up.

I think the BDC sector is much more attractive today than we’ve seen in a long time. We had weeks where we published with zero bullish ratings for the sector and sometimes very few neutral ratings. Those weeks we had mostly a wall of bearish ratings.

You know the worst part about a wall of bearish ratings? Everyone is looking for something to buy! They are rarely looking for someone to tell them to just chill with some cash and some baby bonds and wait for things to improve. Then, when valuations finally improve, many investors are no longer interested in the sector.

Market timing isn’t my thing. I spend more time hunting for the individual shares that represent a better value than peers. I would rather be modeling out future cash flows than trying to predict when people will want to buy everything or dump their portfolio. Can I say modeling future cash flows is fun? Is that too nerdy?

If you’re looking for bargains, this is how they show up. They arrive when everyone has a reason not to want them anymore.

Being Active

I picked up a few equity REIT positions today, but I was also active in the preferred shares and baby bond space. 16.19% of my portfolio right now is in baby bonds and preferred shares I purchased in March 2026. We had quite a bit of cash saved up going into the month. That doesn’t count any capital I already had invested in those names. It is only the value of the shares in that sector that were purchased this month. I won’t be able to add as many new positions over the next month as our cash allocation is dramatically smaller now.

What can we do when the cash position gets small? We can still look to optimize by trading between similar investments at materially different prices. We’ve done that for many years and it’s a great way to enhance performance. Most investors are used to the idea of buying or selling stocks in a sector to look for an advantage. This is more attractive with baby bonds and preferred shares, because there is much greater certainty about future cash flows. It is never going to be perfect certainty, but we’re looking at shares that typically trade in a pretty tight range. A tight range plus large cash flows leads to greater certainty about valuation. It’s the fun of analyzing similar companies, but with lower volatility and big yields.

Read the full article here